Chapter 1 Preface: 4/27/2010

by William Schmidt, Ph.D.

(C) 2010 www.tigersoft.com

EXPLOSIVE

SUPER STOCKS

Chapter 1 Preface: 4/27/2010

by William Schmidt, Ph.D.

(C) 2010 www.tigersoft.com

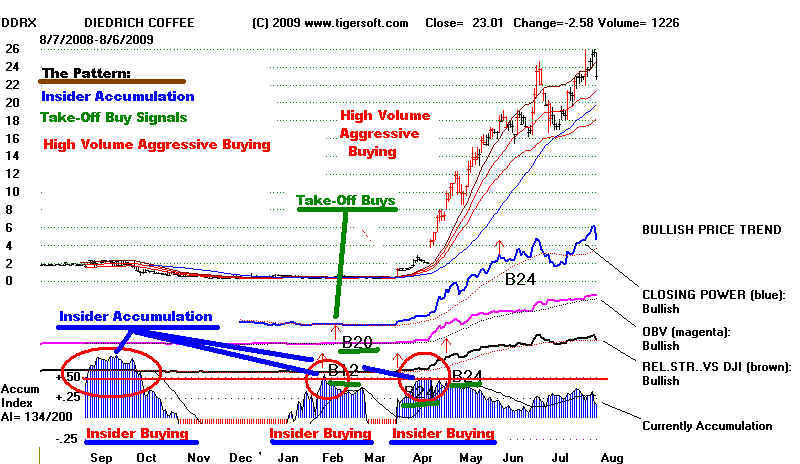

Insider

Buying - The Tiger Advantage

Insiders know their companies better than nearly anyone.

We would well

to watch what they are doing. When you see heavy insider buying

as TigerSoft measures it, do a little "do-dilligence" on Yahoo and

find out how much they are buying, etc. Another useful site is

http://www.insidercow.com/

First, they quietly accumulate all the shares they can.

A weak general

market environment makes this a relatively easy pursuit. See the

tell-tale